Best Travel Credit Cards and Banking for Digital Nomads

Heads up: this post contains affiliate links. If you click and end up buying something, I earn a small commission at no extra cost to you. I only recommend stuff I have actually used or tested, and the commission is what keeps these guides free. Thanks for supporting the site.

By Chenzo | NomadToolsLab

Nothing will drain your travel budget faster than poor banking choices. During my three years as a digital nomad, I’ve made every mistake in the book,overpaying on currency conversions, getting charged ridiculous ATM fees, and dealing with credit cards that were blocked internationally. But I’ve also figured out what actually works.

This guide covers everything I’ve learned about managing money while traveling across multiple countries. From the best credit cards with no foreign fees to multi-currency accounts and ATM strategies, I’ll walk you through the exact banking setup that has saved me thousands of dollars.

Best No-Foreign-Fee Credit Cards

If you still live in the US or maintain a US credit profile, getting a good travel rewards card is essential. Most travel cards charge 3% foreign transaction fees that kill your budget. These don’t.

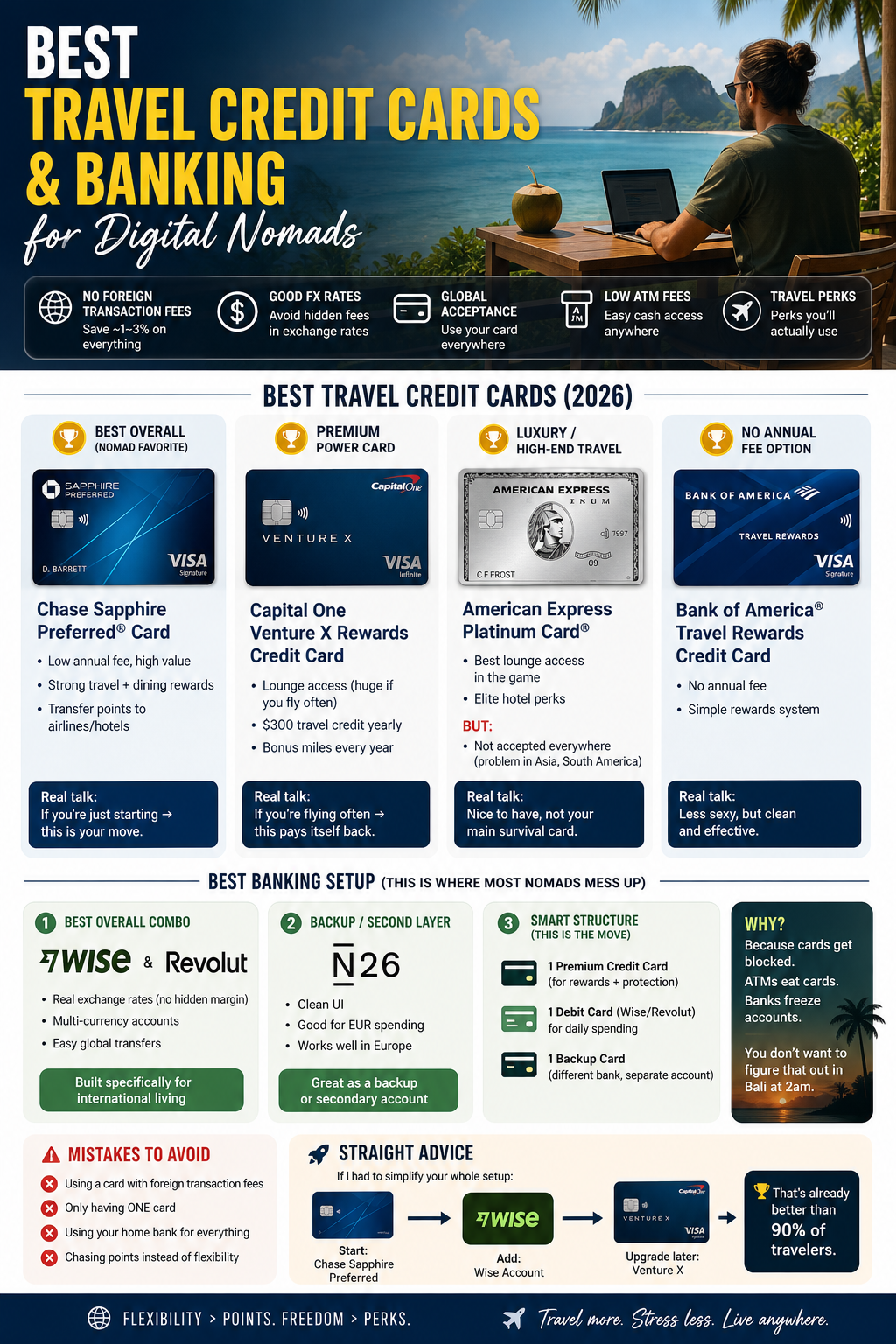

Chase Sapphire Preferred

The Chase Sapphire Preferred is my top recommendation for US-based nomads. Zero foreign transaction fees is the baseline, but the real value comes from the sign-up bonus and points multiplier on travel and dining. I get 2x points on flights and restaurants, 1x on everything else. The $95 annual fee is worth it when you’re spending thousands on flights and accommodation.

Foreign transaction fees: 0%

Annual fee: $95

Best for: Frequent flyers and diners who want points flexibility

American Express Platinum

Amex Platinum is pricier at $695 annually, but if you’re flying premium often, the benefits justify the cost. You get 5x points on flights bought with Amex and 1x on other travel purchases. The Uber credit, hotel credits, and lounge access add real value. Plus, Amex is widely accepted internationally unlike some other premium cards.

Foreign transaction fees: 0%

Annual fee: $695

Best for: High-value travelers who use airline lounges and premium benefits

Multi-Currency Banking: Wise vs Revolut

This is where most nomads lose money,currency conversions. If you’re converting between currencies every week, even a 2% markup adds up to thousands annually. These two services solve that problem.

Wise (formerly TransferWise)

Wise is my primary tool for international transfers and holding multiple currencies. The magic is the mid-market exchange rate,you get the actual rate banks use, not a marked-up tourist rate. I can hold money in 34+ currencies and spend directly without conversion penalties.

Example: transferring $10,000 from the US to Thailand would cost $300 with a traditional bank (3% fee). Wise charges me $50. That’s $250 in my pocket just by choosing the right service.

Transfer fees: 0.5-2% depending on amount

Account fee: Free

Debit card: Optional, about $10 one-time cost

Revolut

Revolut is my favorite for everyday spending. The physical and digital debit cards work everywhere, and currency exchanges happen at real rates. I can instantly convert between 34+ currencies in the app without paying the 2-3% markup banks charge. The app is incredibly user-friendly.

What I love most: no ATM fees in most countries. I can withdraw cash at local ATMs without paying the 3% international fee traditional banks charge. The free tier covers everything I need as a nomad.

Free tier: No fees for most transactions

Premium tier: $7.99-16.99/month for additional benefits

ATM fees: Free up to amount per month on free tier

Wise vs Revolut: Which Should You Choose?

I use both. Wise is better for large international transfers and managing money between accounts. Revolut is better for everyday spending and ATM withdrawals. Here’s my strategy:

1. Transfer money to Wise from my home bank account (transparent fees)

2. Hold it in Wise in the local currency where I’m traveling

3. Transfer to Revolut when I need to spend locally (very low fees)

4. Use Revolut card for shopping and Wise card for ATM withdrawals

Best Banking Options for European Nomads

If you’re based in Europe, you have even better options than American nomads.

N26

N26 is a mobile bank designed for travel. You open the account entirely on your phone with no minimum balance. The card works globally, fees are transparent, and the app is excellent. It’s especially useful for European nomads.

Free tier: No monthly fees, but limited benefits

Premium: EUR 2.99-9.99/month

Monzo

Monzo is a UK-based mobile bank that’s hugely popular with digital nomads. The free version covers everything you need,no ATM fees, excellent exchange rates, spending insights. The design is beautiful and intuitive. If you’re based in the UK or can open a UK account, Monzo is excellent.

Free: Covers most nomads perfectly

Premium: GBP 4.99/month for extra features

ATM Withdrawal Strategies: Avoiding Hidden Fees

ATM fees are where travelers lose thousands. That 3-5% fee on every withdrawal adds up fast. Here’s how I avoid them:

Withdraw larger amounts less frequently

Instead of withdrawing $100 every few days, I withdraw $500 once a week. This cuts my ATM fees by 80%. The only risk is security, but I keep my cash secure.

Use partner ATM networks

Revolut and other banks have partnerships with specific ATM networks. Check the app before traveling to see which ATMs are free. In most countries, I can find 5-10 free ATM options.

Avoid airport ATMs

Airport ATMs charge 5-10% fees. I always withdraw cash from the city before I go to the airport. Sometimes this means planning ahead, but it saves me $50+ per flight.

Decline “dynamic currency conversion”

When you use your card abroad, machines sometimes ask if you want to convert to your home currency. Always choose the local currency. The conversion offered is terrible. Let your bank handle the conversion at real rates.

Crypto-Friendly Banking Options

If you receive crypto payments for work, traditional banks make it difficult. These services bridge that gap:

Wise now allows crypto transfers to fiat, making it easier to get crypto earnings into your account without middlemen. Revolut also accepts crypto deposits and converts to fiat.

International Money Transfer Tips

How you move money between countries matters significantly. Here are my best practices:

Always compare fees between services

A 0.5% difference might not sound like much, but on a $5,000 transfer, that’s $25. I always check Wise, Revolut, my bank, and PayPal to see who offers the best rate.

Transfer in large amounts when possible

Fees are typically percentage-based, so transferring $10,000 once is cheaper than transferring $2,000 five times. The fixed cost per transfer is tiny compared to the percentage fee.

Monitor exchange rates

Exchange rates fluctuate daily. When I’m planning a large transfer, I check if the rate is favorable. If the rate is historically low, I wait a few days.

Banking Solutions Comparison

Here’s a detailed comparison of the major banking solutions for nomads:

Service

Transfer Fee

ATM Fees

Currencies

Wise

0.5-2%

Free with card

34+

Revolut

N/A

Free (limit)

34+

N26

Varies

1.70%

2+

Monzo

N/A

Free

2+

My Complete Nomad Banking Setup

For complete financial freedom while traveling, here’s the exact setup I use:

Primary account: Wise

This is where I keep most of my traveling money. I can hold it in multiple currencies without conversion fees. Zero surprises on exchange rates.

Daily spending: Revolut

I use the Revolut card for restaurants, shops, and online purchases. Zero foreign transaction fees and excellent exchange rates.

Credit card backup: Chase Sapphire

I carry my US credit card for large purchases and as a backup. Also helpful for building credit at home and earning points.

Cash emergency fund: Local currency

I always keep 2-3 weeks of living expenses in local cash as an emergency fund. This covers me if my cards stop working.

Final Thoughts: Banking is Your Secret Weapon

Most digital nomads focus on finding cheap flights and accommodation, but they ignore banking entirely. This is where you lose thousands of dollars annually.

Getting your banking right is one of the highest-return optimizations you can make. The setup I’ve shared here has saved me over $10,000 in my first three years of nomadic travel. You don’t need complicated accounts or multiple cards,just the right tools used strategically.

Start with Wise and Revolut. Get a no-foreign-fee credit card as backup. Understand ATM fees. From there, you’ve solved 95% of your financial challenges as a nomad.